Ultra-large container vessels are coming to West Africa. There is pent-up demand for goods in West Africa and throughout the continent. That’s because African economies are slowly improving, creating more consumers and businesses with money to spend.

Infrastructure to handle the ULCVs has been in short supply, but after considerable investment over the past few years, the giants can now land in numerous African ports.

With the impending container charges imposed by the US on containers arriving at its shores, more carriers and shippers are looking for ways to avoid landing in the US. Increasing West African trade is a natural way to use that capacity.

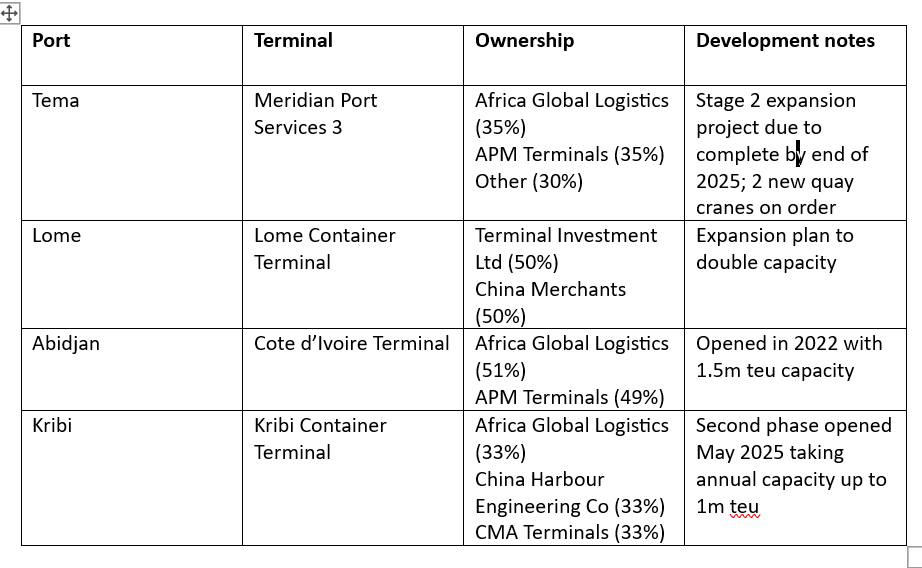

MSC is a major player in this trade. Their situation is helped by the fact that MSC has partial interests in port terminals in key West African locations, as the table below from the article shows. Tema is located in Ghana, Lome in Nigeria, Abidjan in Cote d’Ivoire, and Kribi in Cameroon. MSC has investments in Africa Global Logistics, which operates terminals at three of these ports; and a share in TIL, which has a terminal in Lome.

It’s good to see West Africa getting better access to the world’s goods. Trade improves the lives of both partners, exporter and importer.

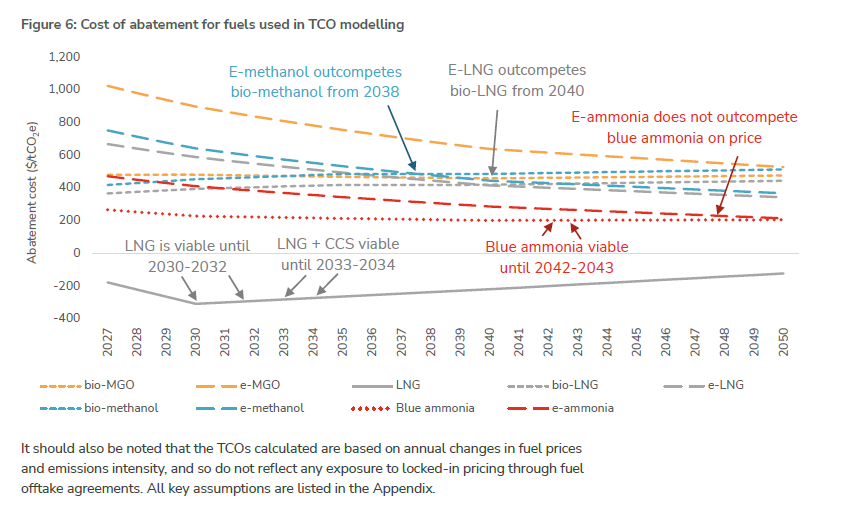

University College London has published a new study considering in detail how shipowners can comply with the IMO rules for carbon emission compliance. It’s very detailed and takes into account not only the different technologies available, such as methanol and LNG, but also the timing of implementing the various regulations. One has to consider all these factors over the 25 or so years of the lifetime of a ship.

Granted, new technologies and availability of different fuel choices can change from what we can see now, but this impartial study favors ammonia-powered ships over the longer time frame. They suggest dual-fuel ammonia ships might be the best bet for investors in new shipping.

“Although there are significant complexities and uncertainties in what was agreed [at IMO MEPC 83] in April, even conservative projections of how remaining policy details will be finalised results in a ‘no brainer’ choice for shipowners in dual fuel ammonia,” said Dr. Tristan Smith, Professor of Energy and Transport at the UCL Energy Institute.

This figure from the report indicates when different fuel choices become cheapest in terms of abatement cost. It seems that e-ammonia never outcompetes blue ammonia before 2050. And LNG remains viable for quite a while, especially with integrated carbon capture.

There are a lot of assumptions in any such study, and the IMO could change the rules in the meantime. But shipowners should be thinking hard about ammonia, and so should international bunker fuel providers.

Update 6/5/2025: Fortescue is jumping on the dual-fuel ammonia bandwagon, and has some not-so-polite comments about others in shipping sticking with LNG.

We now have the latest State of Logistics Report from Penske and Kearney in cooperation with the Council of Supply Chain Management Professionals (CSCMP). It’s a good piece of solid research. I was most interested in two specific aspects it presents.

The first topic was the total United States Business Logistics Costs (USBLC) table. Logistics costs in 2023 actually shrank by 11% over the past year, 2022. That’s a big drop.

First we should note that Motor Carrier costs dwarf all the others, at $937 billion. That’s because in the US Motor Carrier is by far the largest mode of transport, by just about any measure, roughly an order of magnitude greater than the others. It dropped by around 8% from 2022, not the largest drop, which was Water transport. Rail and Parcel held about even, and pipeline went up.

The second largest category of costs is not even a cost of movement; the financial cost of inventory storage at $302 billion. All the carrying costs dropped around 8% from 2022 to 2023.

The third largest category of costs is Parcel at $215 billion. Parcel is driven by e-commerce movements, both business-to-business and business-to-consumer. Parcel costs were holding steady, not a surprise since they have a big labor component, and wages were rising. We’ve all heard of new labor agreements with UPS and Fedex, raising wages substantially.

We noted a large percentage increase (14%) in Shippers’ administrative costs, the largest increase of any category. With all the talk around AI and using computers to relieve administrative paperwork burdens, we don’t see any efficiency realized in the costs. True, logistics is not considered a pioneer industry in adopting technology. It’s probably because logistics is about coordination and cooperation, the hardest problems for computer technology to crack. To make the gains from technology, you have to capture the people doing the work and convince them that things will be better with the technology, that you can make improvements or savings you couldn’t before. It’s a hard sell in many logistics operations.

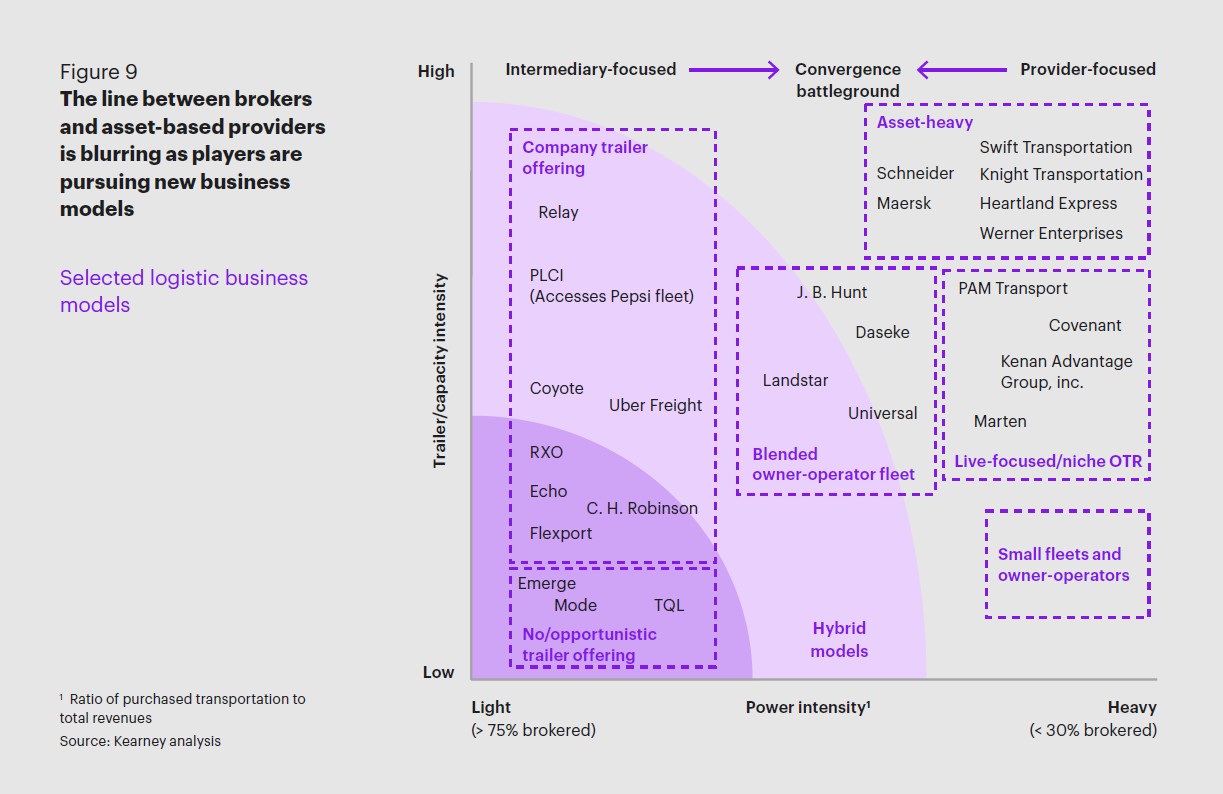

I also enjoyed the discussion of trends in the 3PL sector. The analysts pointed to a move by a number of firms into more asset-heavy logistics. In the 3PL sector that means investing in equipment, such as chassis and containers, or in warehouse space, or occasionally in actual trucks. Figure 9 from the report shows the pattern. In the 2023 time frame, why was this happening? Is it a strategy shift by 3PLs? What’s changing to cause it?

In the press release interview, the commentators were pretty clear. Historically there have been swings from more assets to fewer assets in the 3PL world. They view this as just another cyclical trend.

I agree that it’s cyclical. But what causes the cycles? I think it’s a result of the 3PLs seeking more control over their offerings to customers. If you can’t get containers or chassis from the ocean carriers or rail carriers, you need to be able to provide them for your customers. The large disruptions of 2023, and even earlier, especially in the COVID era, made it hard to guarantee you could deliver on the services you promised as a 3PL. Owning some of the enabling resources put you in a position of more control, so you wouldn’t have to disappoint customers.

There were other responses possible of course. A 3PPL could change suppliers, say of transit services, or include new networks. But there would be no guarantee that similar problems would not occur. Owning equipment and resources such as warehouse space could add certainty to offerings that are likely to remain uncertain over the next year or so.

And one thing seems clear. Uncertainty and disruption are likely to remain parts of the logistics scene in the US and worldwide for at least the next few years. Geopolitics is driving that in ways we can’t even anticipate now.

So for a 3PL to add a few assets to reduce the risk seems like a reasonable response to the increased uncertainty in the logistics world today. I’d argue that is what’s behind the drift toward assets in the 3PL world.