India is instituting major improvements in their ports and maritime system. This is crucial, since India is rapidly becoming an important technology and manufacturing center for the world.

Drewry recently put on a webinar about India’s plans.

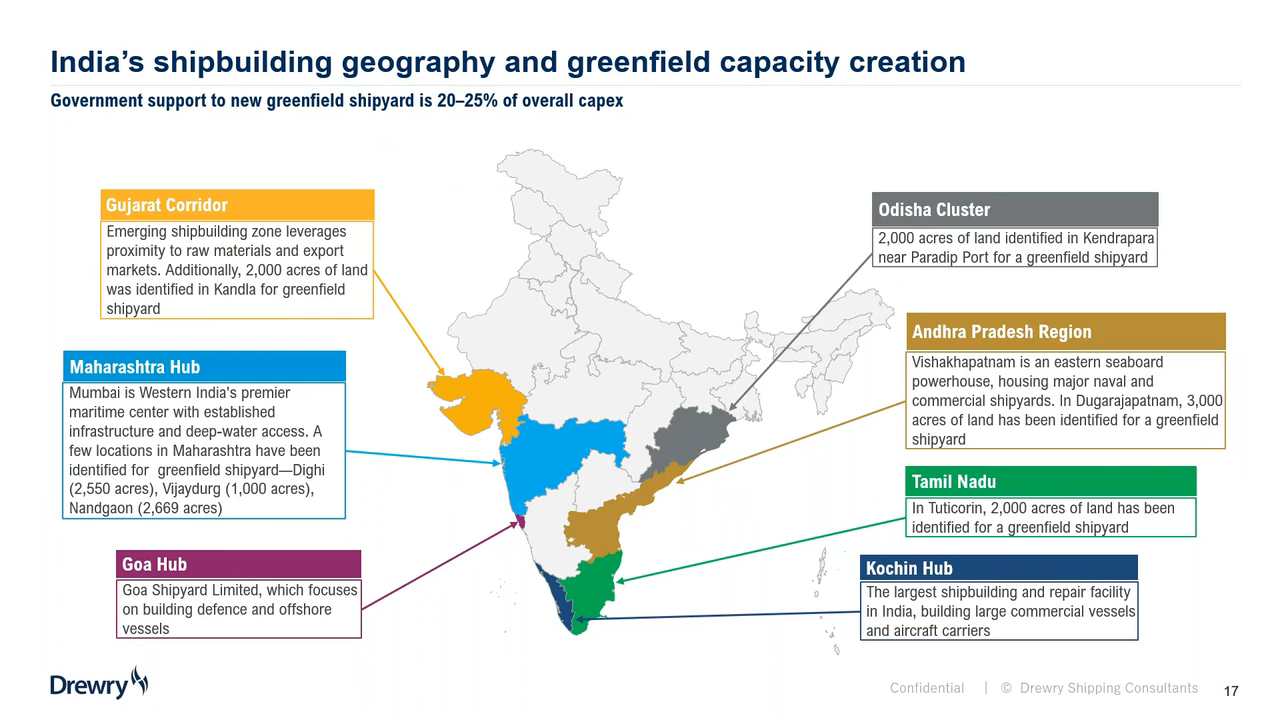

India is taking steps to improve shipbuilding. The figure below shows regions affected.

India is also driving to increase India-flagged ships, and control more ships to carry their production goods. They want to increase the capacity of trade from India, as well as trade to India.

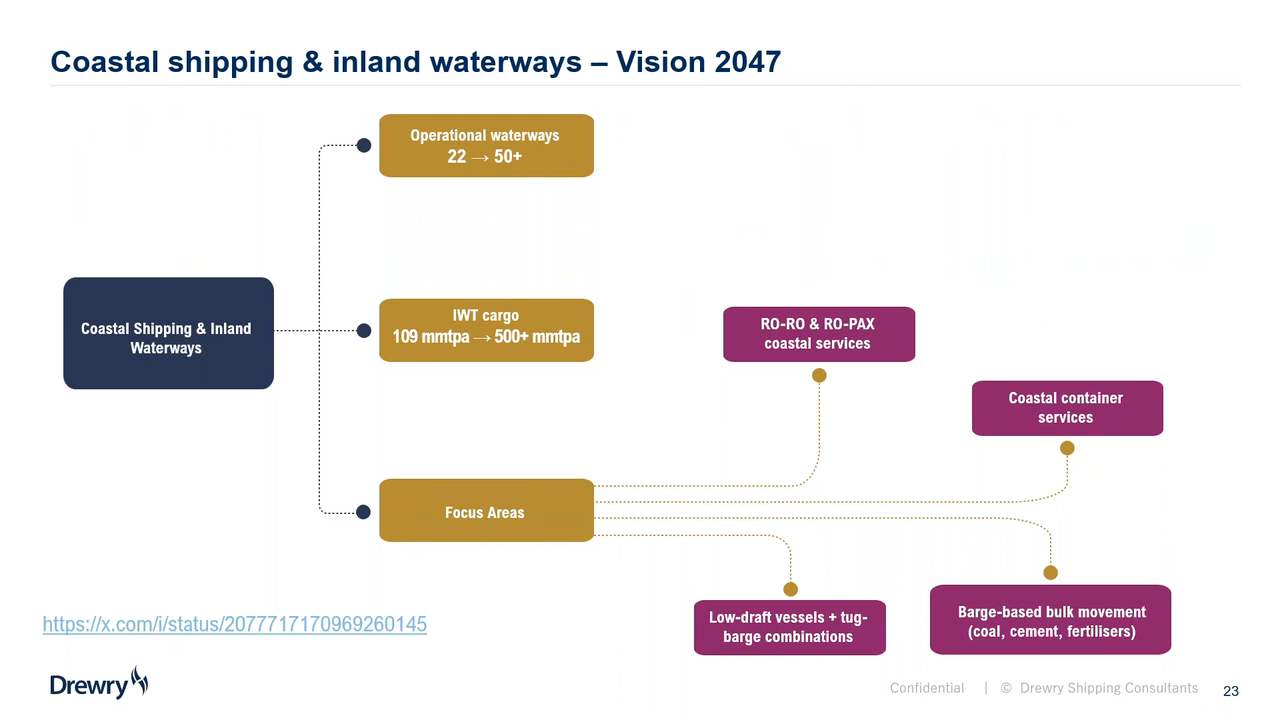

One aspect is improving waterways, including inland waterways. The figure below shows their goals for 2047.

Funding is important. India does not want to make the mistake many countries have made, seeking external capital, for instance from China. That would not be geopolitically smart, since it creates a dependency on a large foreign state and gives that state some control. But India now is generating excess capital looking for investments, because of the fast development in the country. India can do a lot of it themselves, even including private Indian financing. So India is creating financial incentives.

It’s a demanding agenda.

Drewry claims that India should focus on an ecosystem approach rather than individual projects.

With geopolitics favoring India right now as a manufacturing destination, the projects should all work together to create the overall maritime service system the nation needs.