Port Authority of NY and NJ have announced a new container fee payable by ocean carriers. The fee will be levied when the outbound containers don’t exceed inbound containers by 110% in the same period. The port authority also plans to find additional space to store containers near the port, and already has identified 12 acres on the port.

It seems that these two measures are what works to reduce congestion. The same two kinds of measures were invoked at the Port of LA and Port of Long Beach to get ocean lines to start moving empties out. In California, though, the container fees were just threatened; they never were begun. that alone was enough for ocean carriers to start moving containers out.

Perhaps we have found a credible set of options to get container carriers to move those boxes.

Terminal congestion in Europe is high, even though there are fewer containers being handled than a year ago.

Ocean carriers handle congestion by skipping calls, and landing the containers at smaller ports, then sending them by land to their final destination. Skipping calls fouls up schedules for everyone, and makes it impossible to plan for increased capacity. It’s a nightmare situation for port terminal scheduling and for much of the hinterland service logistics, such as barge, rail and truck.

Another source of congestion is containers sitting in ports, often empty, awaiting movement elsewhere.

Almost everyone believes ocean carriers ought to improve on keeping schedules and sailing when they planned, meeting commitments made in advance to the terminals they intend to stop at. When there’s little excess capacity, altering schedules throws all the downstream logistics plans out of whack. It is like a bullwhip effect; when a ship skips, all the efforts planned to handle those cargoes is wasted, and has to be reorganized as best it can for what is believed to be the next round of deliveries. Keeping entire supply chains in a quandary does not lead to efficient logistics in the hinterland.

Ocean carriers are averaging about 30-40% ontime deliveries right now, and their on-time percentage has been excruciatingly low for a couple of years. No land-based logistics service could stay in business with these kinds of numbers.

In order to get ocean carriers to commit to scheduled berthings, ports are going to have to share information about berth window schedules. If this data were more public, comparisons could be made and carriers that routinely missed their slots could be penalized by getting deferred when they wanted to berth elsewhere. Getting liners to commit to berthing schedules requires cooperation among ports.

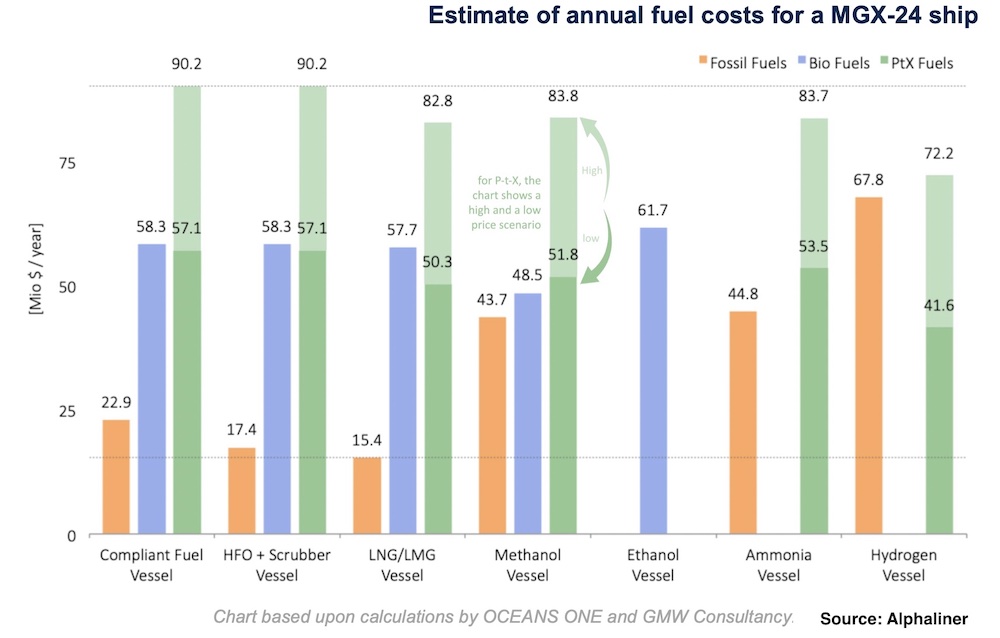

A new technical and commercial comparison of alternative fuels for ocean carriers compares expected bunker costs for different size and differently equipped ships. Alphaliner, a consultancy for ocean carriers, has reviewed that comparison.

Alphaliner’s review shows the ship owner and operator what they can expect in economy over the next few years. The results indicate that as the new regulations for CO2 emissions kick in, fuel costs will become a much larger percentage of total ship operating costs, perhaps double, or even more.

For instance, the graph they publish shows fuel costs for differently equipped Megamax-24 (MGX-24) ships. A megamax-24 ship is typically 400 meters long and 61 meters wide, with a depth of about 33.2 meters. It should carry around 23,500 twenty-foot equivalent (TEU) containers (Alphaliner newsletter).

The graph compares use of fossil fuels, bio fuels, and power-to-fuel (PtX) fuels (read about them). The PtX fuels convert renewable sources such as wind, sun, hydro, and geothermal, to fuel products such as hydrogen, ammonia, or products containing carbon, such as syn-crude. If carbon is used in the PtX process it should be from non-fossil sources or unavoidable industrial carbon emissions capture and reuse.

Source: Splash247 article.

Even bio-fuels cost a lot more than conventional fuels when all the upstream supply chain emissions are considered, for these very large ships.

The graph seems to imply that scrubbers are still a very important technology in the fight to clear the air. And LNG has a role to play, though it might be temporary. At their best, the PtX technologies such as electric-powered ships are comparable to or better than bio-fueled vessels.

There’s clearly a long way to go for ocean shipping to go where it needs to in the race to clean up global emissions.

However, some of these non-fossil technologies will adapt over the next few years, and costs will come down. It’s hard to do much more with the fossil fuel technology.

The argument Alphaliner makes is that soon fixed costs will be a smaller part of the total cost of a large ship than fuel operating costs. As these proportions change, emphasis will come more on building ships with desirable emissions control power systems, since the availability and price of fuel will be driving overall costs.

That’s an interesting point. We will see the extent to which it influences the next generation or two of ship orders.