Here we see a day in the life of a package delivery driver for Veho, which seems to be an enlightened last-mile delivery company that is actively trying to make work friendlier to the driver. The system they have developed tries to take into account driver needs as well as those of the customer and the shipper.

One of the major factors involved in keeping a workforce today is giving workers input and making the workplace friendly for them.

Veho seems to be using that principle to drive their business. Let’s hope it is successful for them.

One downside of this approach is the need for a depot where the packages are brought before the routing is done. That’s a capital expense that not all services will want to implement. It also slows up expansion into new markets, since the warehouse sites must be found and built out. However, the depot is key to the optimization for all the involved parties, including the driver.

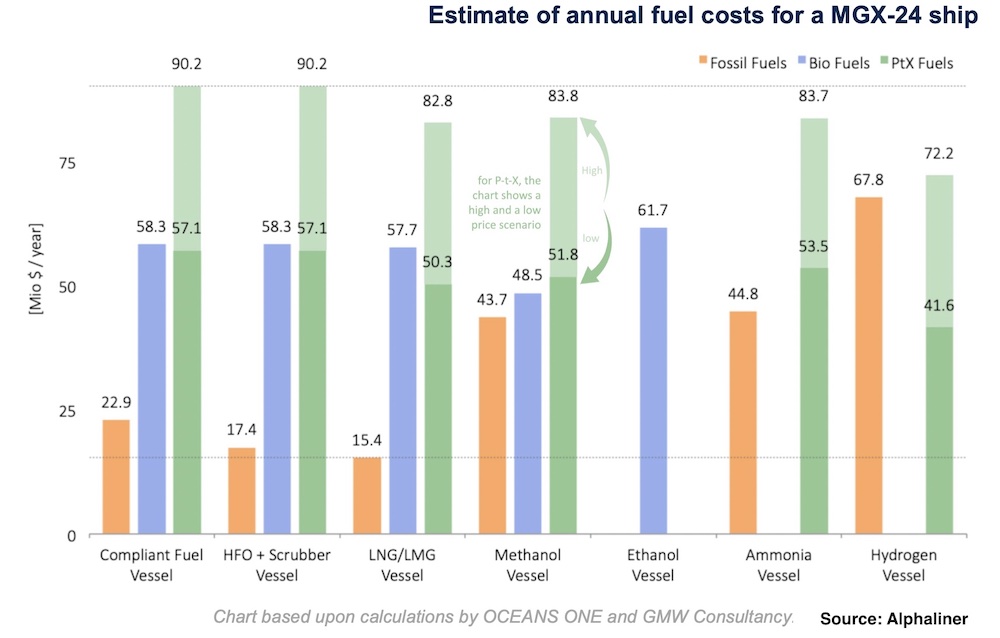

A new technical and commercial comparison of alternative fuels for ocean carriers compares expected bunker costs for different size and differently equipped ships. Alphaliner, a consultancy for ocean carriers, has reviewed that comparison.

Alphaliner’s review shows the ship owner and operator what they can expect in economy over the next few years. The results indicate that as the new regulations for CO2 emissions kick in, fuel costs will become a much larger percentage of total ship operating costs, perhaps double, or even more.

For instance, the graph they publish shows fuel costs for differently equipped Megamax-24 (MGX-24) ships. A megamax-24 ship is typically 400 meters long and 61 meters wide, with a depth of about 33.2 meters. It should carry around 23,500 twenty-foot equivalent (TEU) containers (Alphaliner newsletter).

The graph compares use of fossil fuels, bio fuels, and power-to-fuel (PtX) fuels (read about them). The PtX fuels convert renewable sources such as wind, sun, hydro, and geothermal, to fuel products such as hydrogen, ammonia, or products containing carbon, such as syn-crude. If carbon is used in the PtX process it should be from non-fossil sources or unavoidable industrial carbon emissions capture and reuse.

Source: Splash247 article.

Even bio-fuels cost a lot more than conventional fuels when all the upstream supply chain emissions are considered, for these very large ships.

The graph seems to imply that scrubbers are still a very important technology in the fight to clear the air. And LNG has a role to play, though it might be temporary. At their best, the PtX technologies such as electric-powered ships are comparable to or better than bio-fueled vessels.

There’s clearly a long way to go for ocean shipping to go where it needs to in the race to clean up global emissions.

However, some of these non-fossil technologies will adapt over the next few years, and costs will come down. It’s hard to do much more with the fossil fuel technology.

The argument Alphaliner makes is that soon fixed costs will be a smaller part of the total cost of a large ship than fuel operating costs. As these proportions change, emphasis will come more on building ships with desirable emissions control power systems, since the availability and price of fuel will be driving overall costs.

That’s an interesting point. We will see the extent to which it influences the next generation or two of ship orders.

How do innovations get to logistics and supply chain firms? Here is the current state of the situation.

We went through a period of high venture capitalist (VC) interest in Supply Chain and Logistics startups. but now with some contraction and with high interest rates, the money is drying up. How will firms get money to develop innovations?

As so often in tech, the big question is, hardware or software? Years ago in Silicon Valley that was the intro line used at parties!

Hardware products require more involvement with the actual situation where they will be made or used– a use test bed. They need to be developed near users’ sites. Software products, like scheduling software or logistics management software, can be built anywhere and tested via the internet. They require much less physical user involvement.

And hardware products require immediate feedback from the users as they are being developed. They need to fit, to match the required form factors, and to be able to handle the situations encountered in the location of use. So customers are consulted as you go along, and serviceability is built in as the design progresses. In fact, often the design is the service that is actually being sold. Serviceability is built into the first viable product.

With software, on the other hand, customer service capability is pushed off down the road. It doesn’t become a burden on the firm creating and offering it till there’s a large customer base. And that’s the moment of truth for software-based firms– when they have a large customer base, and the engineers can no longer handle the problems themselves. Normally this occurs more than five years after the first viable product is produced.

This distinction between hardware and software in serviceability makes a substantial difference to VC investors. They normally want to see their investment returns within 5 years, via a public offering or a SPAC or acquisition. With software, they are more likely to be able to cash out before the difficulty occurs. With hardware, the whole development and service framework must be devised before the innovation firm can cash out.

So VCs strongly prefer software investments.

Hardware investments, on the other hand, are often developed as partnerships with user firms, and they have continued oversight as they go along, along with investments. The concerns are going to include how the product is maintained and what service needs it has. And the investments are more likely to come from logistics or material handling firms that have the ability to provide testing sites and engineering oversight for the project. So the investments are more likely to not come from VCs, but from potential clients or users of the hardware.

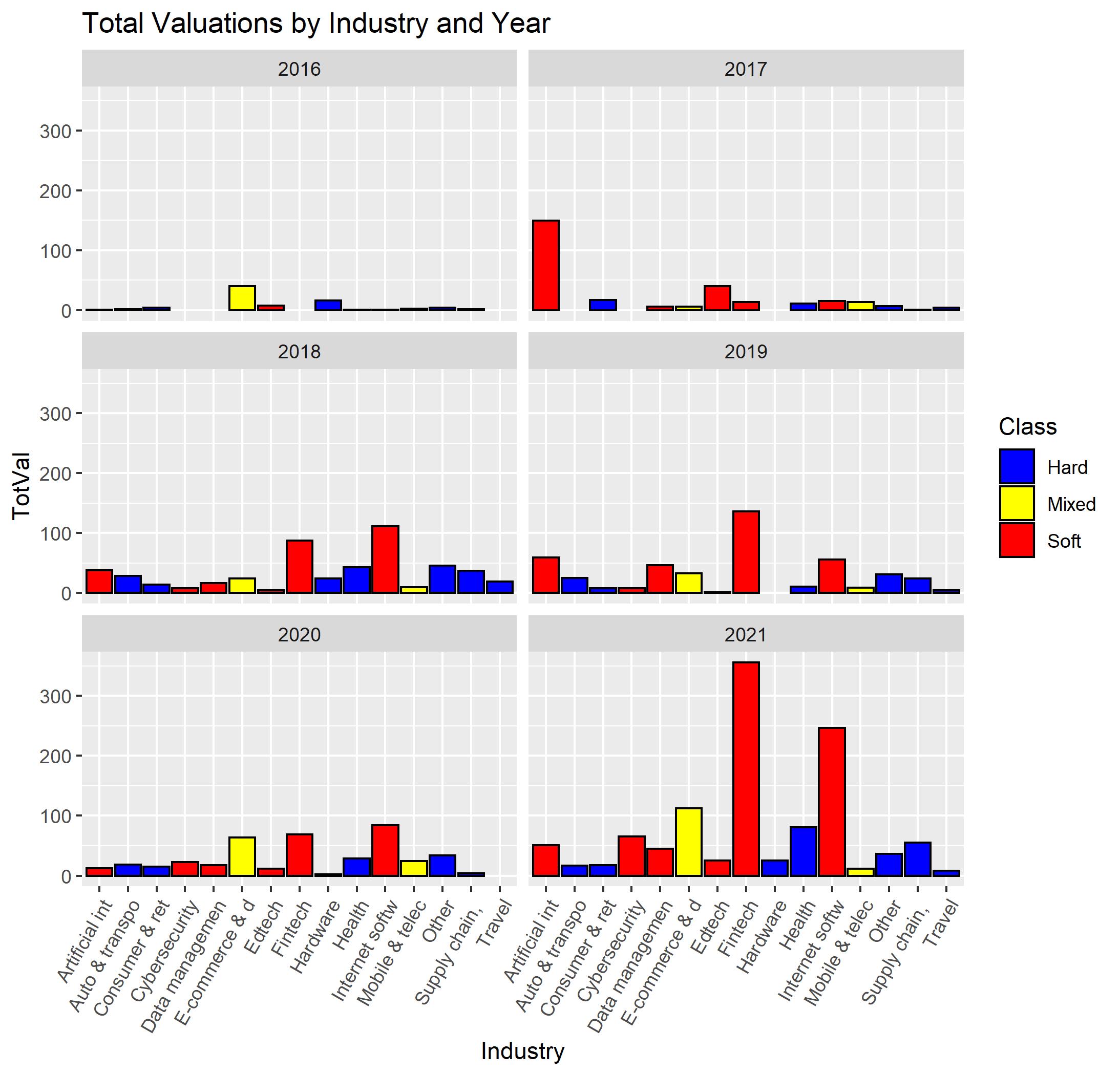

It’s just the way of the world. The graph here shows all the red software investment dominates in most years since 2017. The data is the market valuation of unicorns, firms with over a billion-dollar market valuation, identified by Crunchbase, a firm that tracks startups and innovators and the investors that choose them. Market valuation will give a good idea of the money that can be returned to investors.

Source: Graph by author from Crunchbase Unicorns data.

Notice also the industries favored (the red bars). Supply Chain investments, and Auto and Transportation, are way down the list. The large valuations are in soft industries like Fintech, Internet software, Cybersecurity, and Artificial Intelligence.

VCs know where they can get the returns. Don’t expect them to jump up and support your new electric forklift or container mover.